In the high-stakes hygiene and paper manufacturing industry, your FOB quote is only as stable as the raw material supply chain behind it. For B2B buyers, navigating China’s role as the world’s dominant pulp consumer—importing a staggering 31.111 million tons in 2024—requires a deep understanding of how global fiber dependencies and domestic capacity shifts directly dictate your final landed costs.

This guide deconstructs the “Forest to Mill” journey, providing a strategic analysis of the technical standards for virgin wood pulp from Brazil and Scandinavia versus the rapidly expanding 32 million-ton domestic integrated capacity in China. We will explore the specialized $5.5 billion bamboo value chain, the rigors of FSC/PEFC traceability, and the financial mechanics of cost volatility, explaining why a 10% shift in benchmark pulp prices typically results in a 4–6% fluctuation in your manufacturing production costs.

China’s Role in Global Pulp Consumption

China is the dominant force in global pulp markets, importing 31.111 million tons in 2024. While it maintains a 95% import dependency for coniferous pulp, massive domestic expansion has pushed integrated capacity to 32 million tons, significantly impacting global pricing and supply stability for OEM manufacturers.

Global Import Dominance and Strategic Dependency

China continues to function as the primary engine for global pulp demand, recording 31.111 million tons of imports between January and November 2024. Despite a 6% year-on-year decline in total volume, the nation’s reliance on international fiber remains a critical vulnerability in the supply chain. High import dependence persists for specialized fibers, specifically exceeding 95% for coniferous pulp and approximately 60% for broad-leaved pulp, leaving domestic manufacturers sensitive to international price fluctuations.

The nation’s dominance extends heavily into the recovered paper pulp sector, where it captures 87.27% of global imports, totaling 4,071.61 Ktons in 2024. This volume is essential for fueling China’s extensive recycled product lines. Financial commitment to these raw materials remains substantial, with November 2025 import figures reaching an estimated US$1.873 billion, reflecting the immense capital flow required to sustain the country’s fiber supply chain.

Domestic Capacity Expansion and Market Integration

In an effort to mitigate reliance on foreign supply, China’s integrated wood pulp capacity has doubled over the last four years, now exceeding 32 million tons annually. Projections for 2025 indicate a continued push for self-sufficiency, with an expected capacity growth of 1.6 million tons for broad-leaved pulp and 0.1 million tons for coniferous pulp. These additions are strategically positioned to stabilize local supply and reduce the impact of global trade tensions.

Major domestic infrastructure projects, such as the 1.7 million-ton Liansheng Zhangzhou facility, are specifically designed to counter market volatility introduced by major international providers like Suzano. Currently, the industry is managing a complex balance; while demand for finished paper products—particularly white cardboard and specialty tissues—is growing at 8%, pulp operating rates are averaging approximately 60% as the market absorbs the massive surge in new domestic capacity.

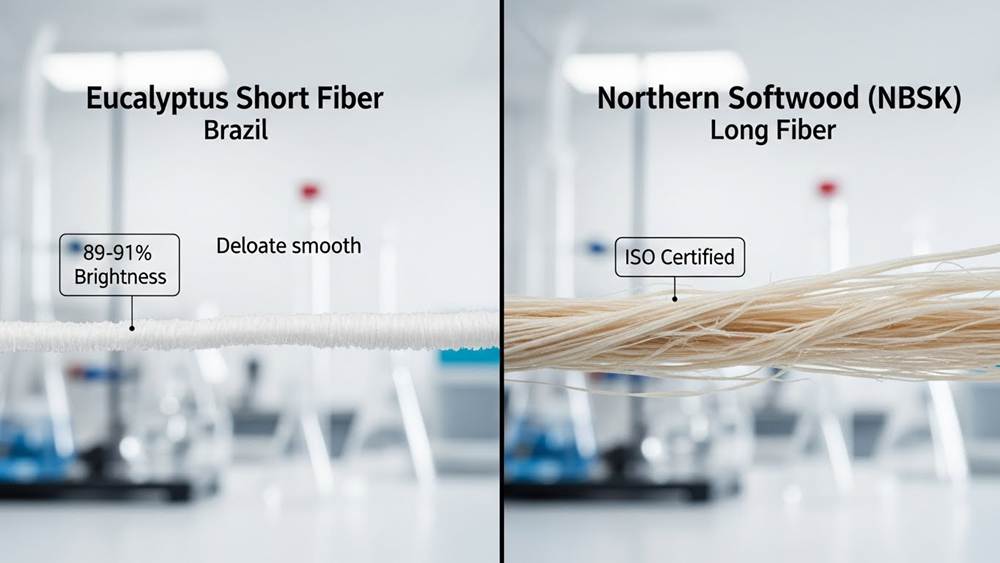

Virgin Wood Pulp: Brazil, Canada, and Scandinavia Connections

Brazil, Canada, and Scandinavia are the primary global hubs for virgin wood pulp, providing the long-fiber softwood and short-fiber eucalyptus essential for high-quality tissue. These regions utilize Kraft (sulphate) pulping—the industry standard for 84% of chemical pulps—to produce fibers that meet strict ISO standards for brightness, purity, and pH stability.

The Global Sourcing Hubs: Why Brazil, Canada, and Scandinavia Lead Production

Brazil has established a dominant position in the global market through its production of Eucalyptus (hardwood) pulp. This specific fiber provides the bulk and surface softness required for premium facial tissues and luxury 3-ply toilet paper. Conversely, Canada and Scandinavia serve as the critical sources for Northern Bleached Softwood Kraft (NBSK), which is renowned for its superior tensile strength and is a fundamental component in high-capacity jumbo rolls.

The efficiency of these regions is largely due to the widespread implementation of the Kraft (sulphate) pulping process. Currently accounting for 84% of the world’s chemical pulping, this alkaline method uses sodium hydroxide and sodium sulphide to dissolve wood lignin while preserving the integrity of the cellulose fibers. By focusing on virgin fiber sourcing, these producers eliminate the risks associated with recycled paper streams, such as lower brightness levels and the presence of physical contaminants or adhesive residues.

Technical Specifications and Quality Standards for Imported Virgin Pulps

Technical excellence in virgin wood pulp is defined by its optical and chemical properties. Full-bleach softwood kraft pulp typically achieves a brightness rating of 89–91% through multi-stage sequences like CEDED or CEHD. To meet modern environmental safety standards, mills implement Best Available Techniques (BAT) to minimize 2,3,7,8-TCDD and TCDF dioxins by significantly reducing elemental chlorine multiples during the delignification process.

In addition to brightness, material purity is strictly monitored via ISO standards. Adherence to ISO 29681 ensures precise pH measurement under low ionic strength conditions, which is vital for the chemical stability of the final tissue product. Producers also maintain strict purity thresholds for metal extractables, limiting cadmium to 0.02 mg/kg, lead to 0.15 mg/kg, and chromium to 0.05 mg/kg. Furthermore, ash content is maintained at a precision of 0.01% or better when tested at 900°C, ensuring a clean and residue-free paper web during the conversion process.

The Domestic Bamboo Supply Chain in Southern China

China dominates the global bamboo sector with a USD 5.5 billion market supported by 6.01 million hectares of forest across 16 southern provinces. Key hubs like Sichuan, Hunan, and Fujian produce over 3.5 million tons of bamboo-based materials annually, driven by a tiered value chain of farmers, traders, and industrial processors under the National Bamboo Plan.

| Province/Region | Production Capacity | Primary Industrial Segment |

|---|---|---|

| Sichuan | 23.47% National Share (>500k tons) | Bamboo-based panels and pulp R&D |

| Zhejiang | 1,081,682 tons | Daily necessities and finished goods |

| Fujian & Hunan | >500,000 tons each | Panels and industrial raw materials |

Regional Distribution and Resource Scale in the Southern Provinces

China’s bamboo sector represents a significant portion of the global industry, accounting for USD 5.5 billion of the total USD 7 billion market. This dominance is underpinned by 6.01 million hectares of bamboo forest coverage, concentrated primarily across 16 southern provinces. Major regions such as Fujian, Zhejiang, and Sichuan serve as the backbone of this resource base, providing the raw material necessary for large-scale industrial applications and high-volume handicraft production.

The geographic concentration of production is highly specialized; Sichuan, Hunan, Fujian, and Anhui are the primary hubs for bamboo-based panels, with each province exceeding 500,000 tons in annual output. In particular, Zhejiang province has established itself as the leader in the “daily necessities” segment, contributing over 1.08 million tons of finished products to both domestic and international markets. This regional specialization ensures a steady supply of diverse bamboo derivatives, from construction materials to consumer goods.

Value Chain Governance and Industrial Processing for Pulp

The industrial value chain is structured through a tiered governance model that begins with smallholder farmers responsible for harvesting shoots and poles. These materials are then channeled through district-level collectors and traders who consolidate supply for large-scale industrial processors. The National Bamboo Plan (2011-2020) has been instrumental in formalizing this structure, prioritizing research and development in bamboo-based pulp as a sustainable, high-yield alternative to virgin wood fiber to ensure long-term timber security.

Despite its scale, the supply chain faces specific regulatory and economic constraints. Forestry regulations strictly prohibit destructive harvesting practices to maintain ecological balance, while provincial taxes and trade fees can impact the overall cost-competitiveness of bamboo materials. However, integrated cross-border processing models, such as the factories located in the Xiengkhor and Ett districts, demonstrate the chain’s sophistication by facilitating the export of specialized bamboo pulp to markets in Taiwan and Southeast Asia.

Build Your Premium Toilet Paper Brand with Expert OEM Solutions

How Pulp Price Fluctuations Impact Your FOB Quote

Pulp fiber represents the largest cost component in paper production; a 10% increase in benchmark pulp prices typically yields a 4–6% rise in mill-gate costs. FOB quotes are further influenced by a 30–60 day index lag and currency fluctuations, often managed through ±2% FX buffers and freight review thresholds.

The Direct Correlation: Fiber Costs and Index Lags

Pulp fiber serves as the dominant cost driver for paper products, where a 10% shift in benchmark prices translates directly to a 4–6% change in finished paper costs. Current pricing is often benchmarked against global indices, such as China BEK at USD 495/t and BSK at USD 695/t, but these figures typically operate with a 30–60 day reporting lag. This misalignment is most pronounced when contracts utilize “prior quarter average” formulas, which can cause current spot prices to deviate from established FOB rates, creating financial friction between the mill’s output cost and the buyer’s expected quote.

Mitigating Volatility: FX Buffers and Freight Thresholds

To manage market instability, technical FOB contracts incorporate an FX buffer of ±2% to absorb minor currency swings; however, a 5% breach in currency stability can impact landed costs by as much as 3–8%. Beyond raw materials, freight and energy review clauses are triggered by specific thresholds, such as a combined $15/ton increase or a 40% spike in ocean freight from a standard $150/ton base. For effective procurement, evidence-based negotiations rely on “two consecutive prints” of weekly thresholds to filter out temporary market noise from permanent price adjustments, ensuring quotes remain reflective of actual production realities.

Ensuring Traceability: FSC and PEFC Chain of Custody

Chain of Custody (CoC) certification is a traceability mechanism that tracks forest-based materials from the forest to the final product. Using standards like PEFC ST 2002 and FSC CoC, it requires all legal owners in the supply chain to maintain certification; a single uncertified link breaks the chain, disqualifying the product from being marketed as certified.

| Certification Component | Technical Requirement | Compliance Cycle |

|---|---|---|

| Primary Global Standards | PEFC ST 2002 / FSC Chain of Custody | Continuous Verification |

| Surveillance Assessments | Mandatory On-site/Documentation Audits | Annual Frequency |

| Certificate Validity | Full System Re-certification | 5-Year Term (Max) |

| Material Accounting | Physical Separation of Certified Goods | Ongoing Operations |

Foundational Standards and the ‘Unbroken Chain’ Requirement

The implementation of PEFC ST 2002 and FSC Chain of Custody (CoC) Certification Standards provides the rigorous framework necessary to ensure forest-to-consumer traceability. These systems are designed to monitor the flow of forest-based materials through every stage of production and distribution. A critical technical mandate is the requirement for an unbroken chain: if any entity holding legal ownership of the material—ranging from primary sawmills to secondary wholesalers—fails to maintain active certification, the product immediately loses its certified status and cannot be marketed as such.

The scope of these standards is comprehensive, covering all entities that manufacture, process, trade, or sell forest-based products. This includes Original Equipment Manufacturers (OEMs) like Top Source Hygiene, who must integrate these protocols into their broader management systems. Under the PEFC framework, this certification also necessitates the inclusion of management requirements that address vital health, safety, and labor issues, ensuring that the supply chain is not only environmentally responsible but also socially compliant.

Operational Compliance: Audit Cycles and Material Accounting

Maintaining certification requires adherence to strict procedural timelines and operational protocols. A standard CoC certificate is valid for a maximum period of five years, at which point a full re-certification audit is mandatory. To bridge the gap between re-certifications, companies must undergo annual surveillance audits conducted by independent third-party certification bodies. these assessments evaluate on-site facilities, verify staff training records, and scrutinize documentation to confirm that the management systems continue to meet the international standards defined by PEFC and FSC.

Technically, the efficacy of the Chain of Custody relies on precise material accounting protocols. Certified organizations are required to implement physical separation or robust credit systems to prevent the mixing of certified and non-certified materials during production and processing. Furthermore, procurement verification must be conducted using official certified supplier databases to ensure all incoming raw materials are legitimate. Accurate content documentation and comprehensive record-keeping serve as the evidentiary trail necessary to prove compliance during rigorous audit cycles.

Alternative Fibers: The Future of Agricultural Residues

Agricultural residues like banana stems, wheat straw, and bagasse offer a sustainable alternative to wood pulp, yielding 2-7 tons of harvestable fiber per hectare. Through chemical or enzymatic retting, these materials produce high-strength fibers—reaching tensile strengths of 458 MPa—that are ideal for biodegradable packaging and specialized paper products.

Extraction Methods and Yield Efficiency of Crop Residues

The transition to non-wood fiber sources relies heavily on the efficiency of extraction processes and harvestable yields. Typically, crop residues provide a harvestable fiber yield ranging from 2 to 7 tons per hectare, which translates to approximately 1 to 3 tons per acre depending on the specific crop variety and local agricultural conditions. These yields offer a significant buffer against wood shortages, integrating seamlessly into circular bioeconomy models by utilizing waste that would otherwise be discarded or burned to alleviate environmental impact.

Among the various extraction techniques, chemical retting stands out as the most efficient industrial method. By utilizing agents such as sodium hydroxide, sodium benzoate, or hydrogen peroxide, manufacturers can produce high-strength, clean fibers in a compressed timeframe of just 1 to 2 hours. In contrast, biological and enzymatic retting processes—while environmentally favorable due to the use of pectinase or xylanase—require a significantly longer duration of 12 to 24 hours and often result in materials with lower inherent fiber strength. To bridge the gap for large-scale pulp applications, mechanical extraction techniques like steam explosion and high-pressure homogenization are frequently combined with chemical treatments to maximize the volume and quality of the output.

Technical Performance and Logistical Constraints of Bio-Fibers

The technical viability of alternative fibers is demonstrated through impressive performance metrics across various agricultural species. Banana pseudo-stem fibers, for instance, exhibit exceptional high-performance metrics, including a tensile strength of 458 MPa and a modulus of 17.14 GPa, making them suitable for high-durability applications such as ropes and specialized paper products. Similarly, bagasse-based composition panels can achieve a specific gravity of 0.25, meeting the commercial standards for particleboard when treated with 7% urea formaldehyde resin and 1% wax addition. These bio-fibers provide inherent physical advantages over lower-grade recycled pulps, including superior tear resistance, natural fire resistance, and complete biodegradability.

Despite their technical strengths, logistical constraints remains a critical factor in the scalability of agricultural residue supply chains. Low-density panels produced from cereal straw via continuous extruder processing have a bulk density limit of approximately 135 kg/m³. This physical characteristic restricts the economically viable supply radius to about 25-35 km from the processing facility to maintain feasibility. To maintain commercial standards, biorefinery integration is essential, ensuring that the processing of materials like corn cobs or wheat straw occurs close to the point of harvest, thereby minimizing transportation costs and maximizing the sustainability of the supply chain.

Final Thoughts

Navigating China’s raw material supply chain requires a nuanced understanding of the delicate balance between high import dependency and the rapid expansion of domestic infrastructure. While the nation remains the primary engine for global pulp demand, the strategic doubling of integrated wood pulp capacity and the formalization of the southern bamboo sector are fundamentally shifting the market dynamics. For international procurement teams and OEM partners, success depends on recognizing that sourcing is no longer a simple commodity purchase, but the strategic management of a complex ecosystem ranging from high-tensile Northern softwoods to sustainable, rapidly renewable bamboo reserves.

Ultimately, the future of the fiber supply chain lies in the integration of transparency and technical innovation. As market volatility persists through index lags and shipping disruptions, the adoption of rigorous FSC and PEFC certifications—alongside the exploration of agricultural residues—will be critical for long-term stability. By aligning with manufacturers who prioritize these traceability standards and understand the specific mechanical properties of diverse bio-fibers, brands can secure a resilient supply chain that meets both the premium quality demands of the consumer and the evolving environmental mandates of the global market.

Frequently Asked Questions

Does China produce its own wood pulp for toilet paper?

Yes, China is a significant producer, with wood pulp production reaching 26.9162 million tons in 2023. This domestic supply primarily serves as integrated factory-use pulp to support the growing downstream demand for household paper products.

Why are Brazil and Canada the top suppliers for Chinese mills?

Brazil offers the world’s lowest production costs for bleached hardwood pulp (approx. $740–$750/ton) due to fast-growing eucalyptus cycles (7 years). Canada provides essential Northern Bleached Softwood Kraft (NBSK) pulp; together, they account for nearly 40% of international pulp exports to China.

How does the factory ensure the pulp is from a legal source?

Factories utilize third-party certifications including FSC, PEFC, SFI, and LegalSource. These frameworks require rigorous due diligence, including supply chain information gathering, on-site audits, and risk assessments to exclude illegal timber from the production process.

What is the impact of global shipping on raw material costs?

Global shipping disruptions caused ocean freight rates to skyrocket from $1,500/FCL in December 2023 to over $7,000/FCL by mid-2024. These 400%+ increases, driven by geopolitical route diversions, directly inflate manufacturing production costs and delay raw material procurement.

Can I request a specific fiber blend (e.g., 70% short/30% long)?

Yes, specific fiber blends are common for optimizing strength and softness. However, requests should be made using engineering specifications—such as fiber length (1.0–3.5 mm) and fines content (5–15%)—rather than simple ratios to ensure the pulp recipe meets specific mechanical property targets.

How does bamboo harvesting support local farmers in China?

Bamboo cultivation provides a sustainable livelihood for approximately 7.55 million farmers in China. By selling bamboo timber and shoots without causing deforestation, farmers generate consistent income from a rapidly renewable resource that supports local rural economies.

SEO

Title: From Forest to Mill: Understanding the Raw Material Supply Chain in China

Description: Pulp supply chain dynamics in China dictate FOB costs through import dependency and domestic expansion of the $5.5B bamboo value chain sector.

URL: china-pulp-market-supply-chain-guide

Keywords: Pulp supply chain