Skip to content

Skip to content ")

Procurement managers and retail buyers: sourcing facial tissues for Irish stores and corporate accounts means balancing pulp‑price volatility, tight lead times and new EU sustainability rules while protecting margins. You need suppliers that deliver predictable MOQs, verified recycled content and reliable route options for an island market.

This article identifies top manufacturers and bulk‑sourcing routes for Ireland in 2026, compares private‑label and branded approaches, and gives practical benchmarks you can use in tenders and RFPs — for example, typical production lead times of 20–25 days and Asia door‑to‑door planning of 35–50 days, plus supplier examples such as Top Source Hygiene’s ~2,860 tonnes/month capacity. We also cover logistics tactics for Ireland’s island economy, a compliance checklist for CBAM and the Circular Economy Act (adoption in 2026), and market context: the tissue sector is forecast to grow through 2026 and residential demand represents roughly 77% of volume.

The 2026 Rankings: Top 10 Facial Tissue Manufacturers & Suppliers in Ireland

Quick Comparison: Top Picks

| Manufacturer | Location | Core Strength | Verdict |

|---|---|---|---|

| Top Source Hygiene | Mancheng, Baoding, China (Global Shipping) | Toilet Paper, Jumbo Roll Tissue, Kitchen Towels, Facial Tissue, Napkins, Wet Wipes, Diapers | Factory-direct OEM/ODM with very high capacity and global private-label reach; note MOQs and shipping lead times. |

| Aldar Tissues (Zeus Group) | Rathcoole, Dublin, Ireland | Domestic Facial Tissue Converting, Eco-friendly Retail Lines, Kitchen Towels | Undisputed Irish domestic manufacturer with a new €15m facility; ideal for fast onshore fulfillment and strict CBAM/EU compliance. |

| Accrol Group Ireland | Navan, County Meath, Ireland | Private Label Facial Tissues, Major Multi-ply Retail Grocery Contract Packaging | Leading local private label supplier with heavily automated local converting blocks; built perfectly for major grocery contract runs. |

| Essity UK & Ireland | Dublin Hub / UK Sourcing Operations | Premium Consumer Brands (Cushelle, Velvet), Specialized Retail Facial Tissue Blocks | Dominant market supply lines across Irish retail channels; premium brand integration with top-tier technical softness benchmarks. |

| Sofidel UK & Ireland | Dublin Office / Inter-regional EU Sourcing | High-Capacity Private Label Facial Tissues, Eco-Labeled Retail Hygiene Lines | Massive industrial processing presence across the Irish Sea; ideal for multi-tier store brand pipelines with advanced carbon tracking. |

| Northwood Tissue Ireland | Dublin / Institutional Logistics Network | Commercial Facial Tissues, AFH Bulk Disposable Paper Lines, System Dispensers | Premium commercial utility specialist; top recommendation for facility management networks and corporate contracts. |

| WEPA UK & Ireland | EU Sourcing Operations / Ireland Distribution | Sustainable Private Label Tissues, Recycled Fiber Formats | Elite European producer delivering high-volume private label; robust sustainable pulp options that excel under EU circular acts. |

| Metsä Tissue (Europe Operations) | Dublin Office / Nordic Production Sites | Natural-Fiber Branded Tissues (Lambi, Katrin), High-GSM Bulk Runs | Natural Nordic-fiber consistency with reliable industrial roll bases; great for premium institutional accounts with advance safety stock. |

| Lucart Group | Ireland Distribution Channels | Eco-Certified Facial Tissue, Unbleached Natural Fiber Disposables | World-class ecological processing models; excellent alternative for sustainability-driven corporate RFPs and public sector bids. |

| Kimberly-Clark UK & Ireland | Irish Logistics Office / Global Infrastructure | Kleenex Facial Tissues, Professional Grade Wet Hand Sanits | Globally dominant Kleenex brand recognition; premium utility pricing tiers with heavy retail distribution stability. |

Top Source Hygiene

Top Source Hygiene operates as a factory-direct OEM/ODM partner for household paper products from two advanced factories in Mancheng, Baoding. With 30 years of experience, the company focuses on high-volume, customizable tissue production and private-label supply across more than 56 countries. Local execution from its Baoding facilities gives buyers direct access to production oversight, faster on-site decision-making, and tighter coordination between design, tooling, and manufacturing phases.

The operation runs at significant scale, producing roughly 2,860 tons per month of tissue products while offering customization and sustainability options. Factory control reduces layers between buyer and maker, which limits quality surprises and lowers compliance risk through documented quality systems such as ISO 9001, FDA, and FSC options. Buyers should plan around global shipping lead times and common MOQ expectations (typical 1×40’HQ, with regional flexibility) when sizing orders and timelines.

At a Glance:

- 📍 Location: Mancheng, Baoding, China (Global Shipping)

- 🏭 Core Strength: Toilet Paper, Jumbo Roll Tissue, Kitchen Towels, Facial Tissue, Napkins, Wet Wipes, Diapers

- 🌍 Key Markets: Global — North America, Europe, Asia, Africa, South America, Oceania

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Aldar Tissues (Zeus Group)

Aldar Tissues, operating as a key brand within the prominent Irish-owned Zeus Group, runs a world-class manufacturing and converting plant in Rathcoole, Dublin. Following a landmark €15 million modernization investment, this facility positions itself as Ireland’s premier domestic partner for high-speed household and commercial tissue distribution. Maintaining large-scale manufacturing assets on the island allows Aldar Tissues to provide retail buying departments with an agile, nearby supply solution that operates independently of complex cross-channel shipping lanes.

Factory control and regional execution drive their core market value: running automated multi-ply converting lines in Dublin lets them implement strict European safety policies and respond rapidly to sudden retail demand shifts. This direct operational oversight minimizes supply chain risk for Irish grocers, helping teams manage lean inventory points while ensuring full compliance with upcoming national environmental acts and carbon-border regulations across the local region.

At a Glance:

- 📍 Location: Rathcoole, Dublin, Ireland

- 🏭 Core Strength: Domestic Facial Tissue Converting, Eco-friendly Retail Lines, Kitchen Towels

- 🌍 Key Markets: Republic of Ireland, Northern Ireland, UK Commercial Channels

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Accrol Group Ireland

Accrol Group operates dedicated industrial tissue converting and logistics assets in Navan, County Meath, positioning itself as a central private-label partner for major grocery operators across Ireland. The company specializes in orchestrating large-scale retail tissue programs, managing highly optimized multi-ply facial tissue and toilet paper runs that supply store brands for dominant grocery chains. This localized infrastructure ensures that high-volume private label requirements pass through rigorous domestic quality checkpoints before final store routing.

Their operational framework places heavy emphasis on processing speed and specification standardization. By controlling advanced high-speed packaging machinery in Meath, Accrol Group minimizes structural batch errors and streamlines time-to-shelf parameters for major retail clients. This centralized factory control cuts logistical friction across the Irish marketplace, offering supermarket buying departments an agile contract option configured specifically for frequent promotional cycles and high-volume grocery demand.

At a Glance:

- 📍 Location: Navan, County Meath, Ireland

- 🏭 Core Strength: Private Label Facial Tissues, Major Multi-ply Retail Grocery Contract Packaging

- 🌍 Key Markets: Leading Irish retail supermarket groups, national wholesalers

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Essity UK & Ireland

Essity manages a prominent distribution and commercial office infrastructure in Dublin, anchoring its massive premium consumer brand portfolio across the Irish retail and commercial landscape. Sourcing from its deep, integrated network of high-efficiency European paper mills, the company supplies market-leading products under household names like Cushelle and Lotus. This robust regional supply methodology ensures that top-tier softness parameters and specialized multi-ply tissue products remain reliably stocked throughout all major retail networks.

Their industrial scale translates into predictable quality control parameters and rigorous technical standardization. Sourcing from advanced, centrally managed European sites allows Essity to insulate procurement departments from localized material shocks, reducing long-term product delivery risks. While their primary strategy elevates established retail brand properties, their massive shipping frequency and structured regional warehousing network establish them as a vital supplier for tracking high-volume tissue logistics within the Irish market.

At a Glance:

- 📍 Location: Dublin Hub / UK Sourcing Operations

- 🏭 Core Strength: Premium Consumer Brands (Cushelle, Velvet), Specialized Retail Facial Tissue Blocks

- 🌍 Key Markets: Pan-Irish retail networks, major medical wholesalers, institutional buyers

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Sofidel UK & Ireland

Sofidel coordinates extensive tissue supply programs across Ireland via its localized commercial offices and advanced manufacturing assets distributed across the Irish Sea and Europe. The group excels at executing high-volume contract packaging, supplying major Irish supermarket store labels with premium multi-ply box and soft-pack configurations. Sourcing from their highly efficient integrated paper mills guarantees strict adherence to core technical specifications and product properties required by modern buyers.

The company integrates strict ecological indicators directly into its production and winding infrastructure, making it a natural choice for buying entities tracking intense carbon target guidelines. By deploying massive, centrally located processing networks, Sofidel minimizes raw-pulp volatility exposure and protects corporate customers from sudden material cost shifts, ensuring stable pricing parameters across multi-year private label framework agreements.

At a Glance:

- 📍 Location: Dublin Office / Inter-regional EU Sourcing

- 🏭 Core Strength: High-Capacity Private Label Facial Tissues, Eco-Labeled Retail Hygiene Lines

- 🌍 Key Markets: Ireland, United Kingdom, Central European Retail Markets

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Northwood Tissue Ireland

Northwood Tissue services the Irish commercial and away-from-home (AFH) sectors through highly structured distribution loops and dedicated logistics offices in Dublin. Their product architecture focuses entirely on the specific demands of corporate accounts, facility management firms, and high-frequency institutional environments. By providing robust commercial facial tissues, corporate toilet papers, and specialized washing dispensers, they ensure procurement bodies can secure uniform technical properties across high-occupancy sites.

Their operational strategy mitigates supply risks by managing highly consistent conversion parameters and rigid pulp tracking profiles. Sourcing from their automated regional converting hubs lets Northwood provide reliable case-packs optimized specifically for commercial storage networks. This professional channel focus cuts operational ambiguity for facilities contractors, ensuring steady restock patterns even during high-demand business cycles.

At a Glance:

- 📍 Location: Dublin / Institutional Logistics Network

- 🏭 Core Strength: Commercial Facial Tissues, AFH Bulk Disposable Paper Lines, System Dispensers

- 🌍 Key Markets: Hospitality chains, corporate facility networks, medical complexes across Ireland

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

WEPA UK & Ireland

WEPA coordinates substantial private-label tissue pipelines into the Irish retail economy through its extensive European manufacturing grid and dedicated regional distribution touchpoints. The company specializes in manufacturing custom-tailored sustainable store lines, offering advanced recycled and hybrid pulp blending processes that allow grocery buyers to scale their eco-labeled selections. This supply alignment ensures that strict EU circular design expectations are integrated right at the pulp-milling source.

Because WEPA leverages massive centralized converting technology across Europe, retail procurement teams receive highly uniform sheet parameters and structural packaging consistency across high-volume orders. This reliable technical baseline lowers product defect percentages and minimizes arrival delays at major retail hubs, offering Irish grocers a resilient international partner capable of handling long-term own-brand supply commitments.

At a Glance:

- 📍 Location: EU Sourcing Operations / Ireland Distribution

- 🏭 Core Strength: Sustainable Private Label Tissues, Recycled Fiber Formats

- 🌍 Key Markets: Major Irish supermarket groups, eco-conscious corporate suppliers

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Metsä Tissue (Europe Operations)

Metsä Tissue supplies facial tissues to the Irish market from Nordic production facilities and supports local distribution through warehousing in Dublin. They focus on products with natural fiber content and aim to serve both professional and retail channels that require consistent bulk deliveries, positioning themselves as a steady source for customers who prioritize material composition and predictable inventory flow.

By keeping production in the Nordics, Metsä Tissue maintains close factory control over product consistency and the natural-fiber emphasis noted in their range. Local warehousing in Ireland reduces supply friction and lowers delivery risk for recurring orders, but sourcing from Nordic plants can introduce longer shipping lead times when urgent replenishment is needed.

At a Glance:

- 📍 Location: Dublin, Ireland

- 🏭 Core Strength: Facial Tissue, Kitchen Rolls

- 🌍 Key Markets: Europe, Ireland

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Lucart Group

Lucart is an Italian tissue specialist serving Irish wholesalers via EU distribution channels, offering eco-certified and biodegradable facial tissues alongside toilet paper and other eco-friendly lines. The company targets sustainability-driven retailers and HoReCa customers who need compliant, environmentally focused tissue products sourced within the European supply chain. Operating through EU distribution supports local execution for Irish partners by keeping procurement and certification within regional systems and familiar regulatory frameworks.

Lucart’s Italian roots imply close factory oversight and alignment with EU eco-certification processes, which helps reduce product and compliance risk for wholesalers and retail buyers choosing sustainable SKUs. At the same time, the brand’s distribution-focused presence emphasizes wholesale supply rather than direct co-manufacturing partnerships, so buyers seeking hands-on factory collaboration may encounter limits. For Irish wholesalers and outlets prioritizing sustainability, Lucart provides ready-made, certified tissue options that fit retail shelves and HoReCa needs while keeping sourcing managed within an EU distribution model.

At a Glance:

- 📍 Location: Ireland Distribution Channels

- 🏭 Core Strength: Facial Tissue, Toilet Paper, Eco-friendly lines

- 🌍 Key Markets: Europe, Ireland

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

Kimberly-Clark UK & Ireland

Kimberly-Clark supports premium facial tissue placement across the Irish market through its primary corporate structures and regional distribution hubs. The company focuses on delivering high-end consumer and commercial variants, placing lotion-infused and ultra-soft sheet structures onto retail shelves under the globally recognized Kleenex brand. This systematic distribution approach ensures that high-margin tissue variants remain readily accessible for both retail chains and bulk B2B traders.

Their large-scale European production lines provide strict manufacturing consistency and rigorous fiber checks across every batch. By routing inventory through highly synchronized supply networks, Kimberly-Clark minimizes logistical gaps across its core lines, supporting predictable reorder parameters for wholesale accounts. While their baseline structure features premium pricing profiles, their reliable market integration makes them a fundamental supplier block across Ireland.

At a Glance:

- 📍 Location: Irish Logistics Office / Global Infrastructure

- 🏭 Core Strength: Kleenex Facial Tissues, Professional Grade Wet Hand Sanits

- 🌍 Key Markets: Ireland, Europe, Global

Why We Picked Them:

| ✅ The Wins | ⚠️ Trade-offs |

|---|---|

|

|

The Irish Tissue Market Outlook: Resilience and Growth in the Hygiene Sector

The Irish tissue and hygiene paper market is expected to grow through 2026, led by toilet paper volumes and steady gains in paper tissues; residential demand dominates while hygiene awareness, urbanization, higher incomes and e-commerce support premium and private‑label uptake, and key risks include pulp price volatility and rising sustainability compliance.

Market snapshot and key segments

Analysts project a positive CAGR for the overall tissue and hygiene paper sector in Ireland to 2026, with revenues split across online and offline channels and baseline growth linked to GDP and consumer spending per capita.

Toilet paper accounts for the largest volume share, followed by facial tissues and kitchen towels. Paper tissues show steady revenue growth and maintain a forward CAGR in recent forecasts.

Channel and end‑use mix skew strongly to residential demand—commonly estimated near 77% in some forecasts—while commercial demand is concentrated in hospitality, institutional and facilities management segments.

Drivers of resilience and near‑term growth

Rising hygiene awareness and ongoing sanitation improvements drive baseline consumption across tissue categories, supporting demand even during inflationary periods where value growth has at times outpaced volume.

Urbanisation, rising disposable incomes and expanding e‑commerce raise penetration and create room for premium and convenience formats. Retailers and wholesalers report stronger private‑label interest where consumers trade down on branded SKUs but still demand quality.

Active competitors in the Irish market—including SCA/Essity, Procter & Gamble, Kimberly‑Clark, Unicharm, Hengan, Sofidel and Metsä Tissue—support innovation, scale manufacturing and broad distribution, which keeps product development and supply availability moving.

Risks, supply constraints, and sustainability trends

Pulp price volatility remains a primary margin pressure because pulp is the main raw material for tissue products; sudden input cost swings compress margins for producers and private‑label buyers alike.

Sustainability trends favor recycled fibre and eco‑friendly materials; forecasts show recycled content holding a leading position in raw material mixes and buyers increasingly require certified options such as FSC.

Premiumisation and hygiene‑led upgrades create sales opportunities but raise sourcing and cost pressures for retailers and private‑label manufacturers. Importers and suppliers must balance cost efficiency with compliance to EU and Irish rules (for example, CBAM, CSRD and forthcoming circular economy measures) when planning sourcing and product strategies.

The Private Label Advantage: How Irish Retailers are Optimizing their Sourcing

Private label lets Irish grocers protect margins and build loyalty by offering tiered ranges (value to premium), tighter supply control through local contract manufacturers and global OEMs, and sourcing terms that balance MOQ flexibility, predictable lead times and strict compliance to EU sustainability and hygiene standards.

Why private label matters for Irish grocers

Private label drives market share and repeat purchase. Dunnes Stores’ Simply Better supports its 22.2% market share and 3.6% year‑on‑year growth, while Tesco’s own labels contribute to roughly 22.0% share. Retailers use store brands to reduce reliance on national brands in commodity categories.

Own‑label lines outpace branded ranges in high‑growth premium segments: private‑label premium ranges clock growth near ~16.3% versus ~8.2% for branded lines, giving retailers margin uplift and on‑shelf differentiation without national‑brand pricing.

Discounters and mainstream chains both exploit private label: Aldi’s Specially Selected, Lidl’s Deluxe and Dunnes’ Simply Better target shoppers across price and quality bands so retailers capture multiple shopper segments within the same category footprint.

Supplier models, capabilities and compliance

Retailers combine local Irish private‑label producers with global OEM/ODM partners to balance speed, cost and scale. Local producers deliver shorter lead times and easier specification changes; global partners add scale and lower unit cost for high‑volume SKUs.

Irish private‑label manufacturers offer end‑to‑end development: formulation/specification, converting, traceability and export readiness. Many participate in Origin Green or similar sustainability programmes to meet retailer ESG requirements and EU reporting needs.

Example — Top Source Hygiene: operates two factories, with roughly 2,860 tonnes/month capacity, ISO 9001 and FSC options, and private‑label ranges from toilet paper to facial tissues. Retail buyers lean on such suppliers for flexible GSM/ply choices, co‑packing and FSC or equivalent credentials for eco‑labelled tissue lines.

Compliance matters at contract stage. Retailers require EU hygiene standards where applicable, FDA approval for products with US market exposure, and chain‑of‑custody or recycled‑content verification to mitigate CBAM, CSRD and forthcoming Circular Economy obligations.

Practical sourcing tactics Irish retailers use

Use a three‑tier private‑label architecture: entry value, dependable mid‑range, and a premium line. That segmentation lets buyers allocate SKU space, pricing and promotional strategies to match customer elasticity across stores and channels.

Negotiate flexible MOQs and sample policies. Suppliers such as Top Source commonly quote a one 40’HQ container MOQ but provide smaller‑order options and free stock samples (stock samples 2–3 days; custom samples ~10 days) to validate quality before committing to production.

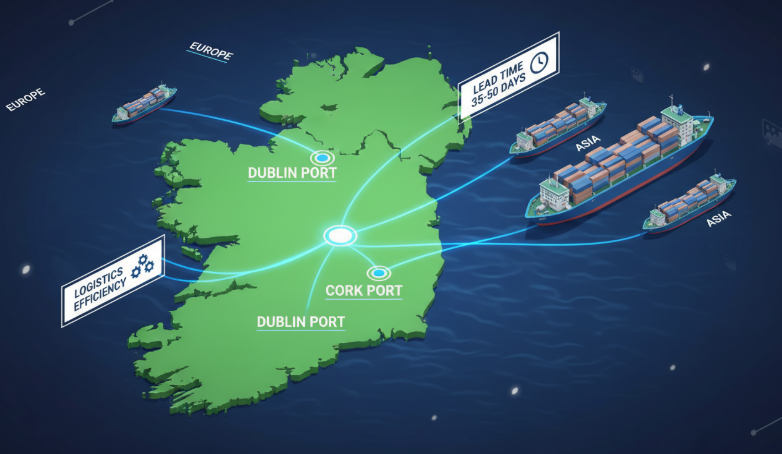

Control lead times and logistics windows to reduce stock risk. Typical production lead times sit at 20–25 days; regional shipping estimates used in planning include Europe 7–14 days and Africa 15–25 days. For Asia‑sourced volumes, plan for longer ocean transit and clearance in total lead‑time modelling.

Use supplier services to speed time‑to‑shelf: request custom branding, tailored GSM/ply and co‑packing at source to avoid retailer‑side rework. These services shorten the store‑ready timeline and reduce warehousing handling costs.

Set commercial and contractual levers: standard payment terms often use a 30% deposit and 70% balance, but buyers negotiate staged payments tied to inspection milestones, enforceable quality KPIs, agreed test protocols and penalty clauses to protect supply continuity.

Operational best practice: embed analytics and supplier scorecards to monitor fill rates, lead‑time variance and quality incidents; use these KPIs to adjust order cadence, safety stock and alternative sourcing lanes when constraints appear.

Top Source Hygiene — Global OEM/ODM Toilet Paper Partner

Logistics Strategy: Managing Supply Chain Efficiency for Ireland’s Island Economy

Focus on visibility, route-aware planning, and flexible inventory policies. Monitor port and ferry links with analytics, optimize routes around ferry schedules and gateway congestion, invest in WMS/TMS and IoT, and keep contingency plans that diversify carriers and modal options while meeting Irish and EU sustainability and customs rules.

Island-specific constraints and strategic priorities

Ireland’s island geography creates tight dependencies on a few seaports and ferry corridors, limited inland redundancy and pronounced seasonal demand swings for coastal and island communities. These factors raise the impact of any port delay or single-route outage, so plan capacity and buffers with that concentration in mind.

Use data and analytics to track transportation routes, berth and quay congestion, warehouse utilization and inventory levels tied to key Irish gateways. Combine historical port-call data with near‑real‑time telemetry from carriers to detect slowdowns early and quantify the cost of rerouting or expedited transits.

Raise supply chain visibility end-to-end so teams spot bottlenecks before they cascade. Visibility reduces emergency decisions at the last mile, helps balance lean inventory with resilience, and shortens time to enact alternate routing when ferry schedules change or a berth becomes unavailable.

Tactical measures: transport, inventory and distribution

Optimize transportation routes using route-planning tools that incorporate ferry timetables, vessel frequency, fuel costs and gateway congestion windows. Build carrier scorecards that capture average dwell, delay variance and on‑time performance for Dublin, Cork and cross‑channel links so planners can prefer consistently reliable services.

Streamline inventory management with targeted policies: apply JIT for high-turn SKUs where transit is secure, use ABC segmentation to set safety stock by criticality and volatility, and run EOQ models that include multimodal lead‑time variability. For Asia imports, plan for 35–50 days door‑to‑door and size buffers accordingly to prevent stockouts during peak season.

Rework node layouts and flows to minimize handling and dwell. Use cross‑docking at consolidation hubs, slotting optimization in warehouses close to major ports, and consolidation of less-than-container loads to reduce frequency-driven cost. Where footprint allows, maintain small coastal buffer depots to shorten last‑mile legs to islands.

Invest in technology and automation: deploy WMS and TMS to manage orders and carrier selection, add RFID and IoT sensors for real‑time asset tracking, and apply predictive analytics to flag likely delays. Automation lowers processing time at congested ports and reduces manual errors that cause shipment misses.

Collaboration, risk management and regulatory alignment

Strengthen collaboration with suppliers, carriers and port operators through joint KPIs, supplier scorecards and shared real‑time dashboards. Create joint contingency plans and run regular tabletop exercises focused on ferry disruptions, port strikes or severe weather to refine handoffs and cut response time.

Use visibility tools and predictive analytics to detect disruptions early, then trigger pre‑defined recovery playbooks: switch to alternate carriers, reroute via other ports, or increase local batch frequency. Diversify carriers and modal options where possible so a single outage does not halt critical corridors.

Align logistics practices with EU and Irish import, customs and sustainability rules. Track compliance against CBAM, CSRD and the Circular Economy Act requirements when sourcing tissue and paper products; capture embedded carbon and recycled content in supplier records, and report supply‑chain performance via analytics to support procurement and regulatory disclosure.

Sustainability Benchmarks: Meeting the EU and Irish Standards for Paper Imports

EU rules—chiefly CBAM, the European Green Deal, CSRD and the forthcoming Circular Economy Act—mean Irish paper importers must collect verified supplier emissions and recycled-content data, embed carbon-cost scenarios in procurement, tighten traceability and update contracts and lead times to meet carbon-pricing and reporting expectations.

Key EU policies and standards that apply to paper imports

Carbon Border Adjustment Mechanism (CBAM): applies a carbon price to imports with high embedded emissions. For paper and tissue this requires suppliers to provide verified emissions data (scope 1–3 where available) and CBAM declarations for affected shipments.

European Green Deal: Fit for 55 targets and the drive to climate neutrality push buyers toward low-carbon and recycled paper. These policy targets raise market preference for recycled feedstock and energy-efficient production across EU supply chains.

Corporate Sustainability Reporting Directive (CSRD): large companies must disclose supply-chain ESG risks using ESRS. Irish wholesalers that serve large EU customers should expect supplier-level data requests once reporting thresholds apply.

Circular Economy Act (adoption in 2026): will prioritise waste reduction and high-quality recycled content. The Act tightens acceptable paper grades, product design and packaging standards for imports into EU markets.

What the rules mean for Irish tissue importers and wholesalers

Cost exposure: CBAM can raise landed cost for products with high embedded emissions. Procurement models must include carbon-charge scenarios and sensitivity testing to estimate potential CBAM liabilities.

Sourcing shift: buyers should prioritise suppliers that can document verified recycled content, maintain FSC chain-of-custody or equivalent, and demonstrate low-carbon production processes that reduce CBAM risk and appeal to circularity requirements.

Reporting burden: wholesalers supplying large corporates will need granular supplier ESG data to support CSRD/ESRS disclosures. Start collecting supplier metrics now to avoid last-minute gaps.

Product specifications: expect rising market demand for recycled-paper grades, clearer traceability of fibre origin, and stricter limits on non-recyclable packaging and waste content.

Practical compliance checklist for procurement and supply teams

Request verified carbon-footprint data from suppliers, covering scope 1–3 where available, and obtain CBAM-related declarations for each import batch or SKU that may be in scope.

Ask suppliers for ESRS-aligned sustainability metrics or raw-data exports (emissions, energy mix, recycled content) to streamline future CSRD reporting and internal risk assessments.

Verify recycled-content claims and chain-of-custody certificates (for example FSC Recycled or EN standards). Keep supporting test reports and certificates on file and map them to each product SKU.

Include carbon-cost scenarios in tender evaluations and landed-cost models so bids reflect possible CBAM charges and evolving carbon-pricing rules.

Add contractual clauses that grant rights to audit emissions data, require supplier improvement plans with milestones, and specify remedies or penalties for inaccurate sustainability claims.

Adjust lead times and documentation workflows to accommodate additional customs checks, CBAM filings and circularity-related paperwork; update standard operating procedures for arrival, inspection and record-keeping.

Frequently Asked Questions

Who are the largest tissue paper suppliers in Ireland?

Key suppliers identified in the available research include: Aldar Tissues — Ireland’s leading household and commercial tissue manufacturer and converter, part of the Zeus Group, which recently opened a EUR 15 million tissue converting facility in Rathcoole, Dublin; Northwood Tissue Ireland — a top institutional supplier providing comprehensive bulk commercial tissue products and dispensing systems to corporate networks; and major wholesale groups supplying retail grocery store brands across the country.

Is there demand for private label facial tissues in the Irish market?

Yes. Broader market data show steady global growth in facial tissues and rising private label share in hygiene categories. Recent estimates place the global facial tissue market at roughly USD 8 billion with projections near USD 10.3 billion by 2030 at about a 4.4% CAGR. Retailer data and IRI insights point to stronger private label adoption in commodity hygiene items, driven by value-seeking shoppers and retailer investments in store brands. European trends support demand, so Irish wholesalers and retailers can find opportunity in private label facial tissues, especially for value and eco-friendly options.

What are the key EU regulations for importing tissues into Ireland?

For commercial tissue paper and facial hygiene products, key EU frameworks center on timber regulations requiring verified fiber tracing, along with general consumer safety markings. Importers must confirm raw pulp origins via chain-of-custody documentation (such as FSC/PEFC markers) and file necessary declarations under active CBAM schedules to track embedded processing carbon. These rules contrast with medical or clinical standard sets, strictly regulating consumer paper tissue safety, fiber legality, and carbon pricing alignment across the EU border zone.

How long does bulk shipping take from Asia to the Port of Dublin?

Ocean transit from major Asian ports to Europe typically runs 30–45 days. A realistic door-to-door timeline is about 25–60 days, with a practical planning window of 35–50 days to cover pickup, export clearance, vessel waiting, ocean transit, import clearance and last-mile delivery. Typical step times: pickup and container stuffing 1–3 days; export handling 2–5 days; vessel waiting 1–3 days; ocean transit 30–45 days; import clearance and port handling 3–7 days; final delivery 1–3 days. Expect variation from carrier schedules, seasonal congestion and customs delays.

Are there local Irish manufacturers for specialized facial tissues?

Yes, local tissue production is active on the island through specialized domestic facilities like Aldar Tissues (Zeus Group) in Rathcoole, Dublin, which converts and packs versatile household tissue ranges. Additionally, automated regional contract lines like Accrol Group in Navan provide local grocery store programs with massive onshore private label facial tissue finishing. Sourcing from these local multi-ply lines allows Irish retail and corporate buyers to drastically compress delivery timelines and coordinate directly with regional converting managers.

Final Thoughts

Ireland’s tissue market looks resilient through 2026. Strong residential demand, steady toilet‑paper volumes and rising private‑label and premium tissue sales support revenue growth, while global suppliers and local converters keep product availability and product development moving. Key risks include pulp‑price volatility and tighter EU sustainability and reporting rules, which put pressure on margins and complicate sourcing decisions.

Buyers and suppliers should act now: require verified recycled‑content and emissions data, include CBAM and CSRD scenarios in landed‑cost models, and use supplier scorecards to manage quality and lead times. Adopt a three‑tier private‑label approach, balance local contract manufacturing with global OEMs for flexibility, and invest in visibility tools (WMS/TMS, IoT) plus modest buffer inventory so teams can detect and respond to port or ferry disruptions without harming on‑shelf service.